A rare freehold apartment block opposite The Istana is up for sale — and one buyer can own all 26 units

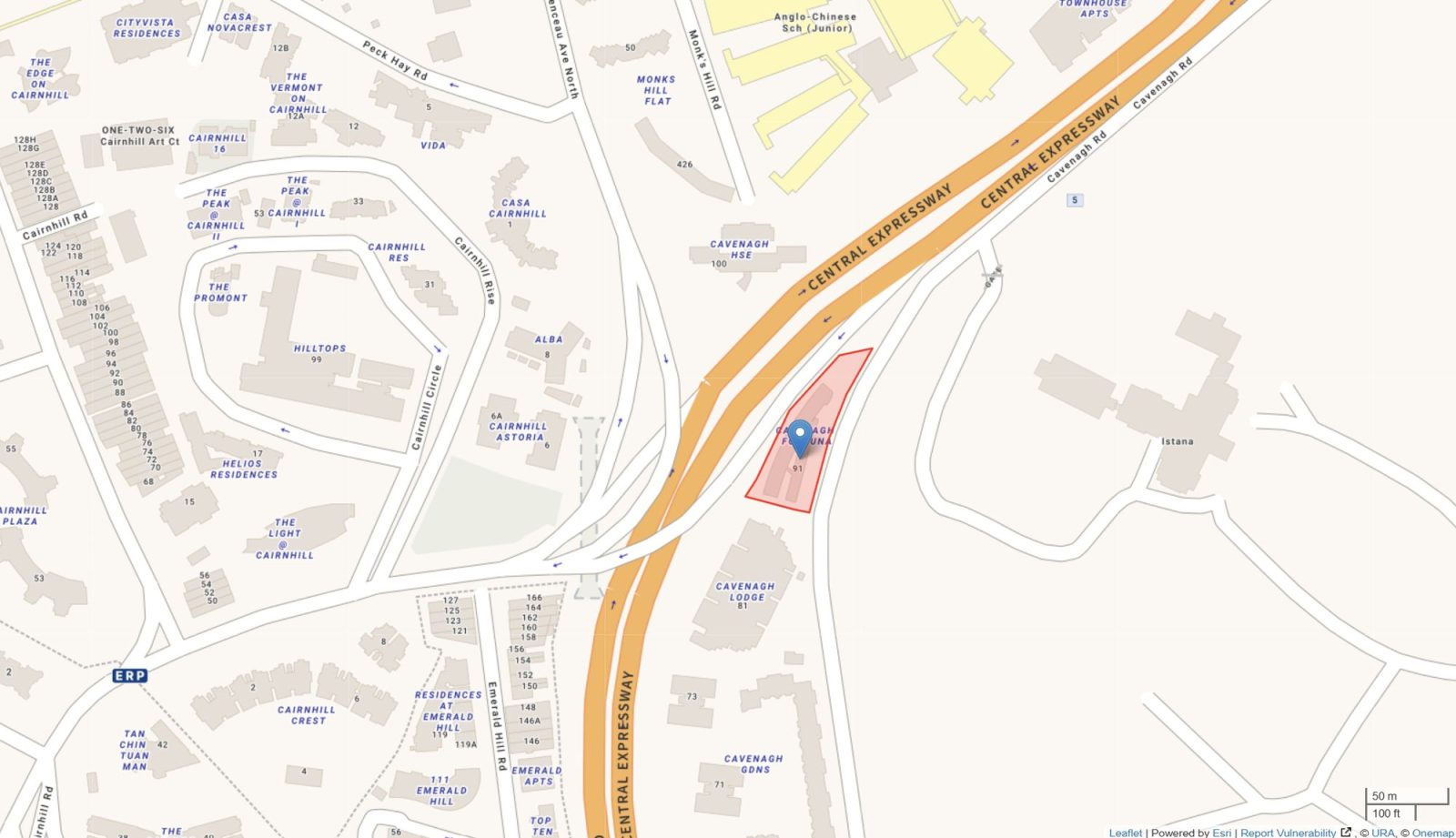

Cavenagh Fortuna sits along Cavenagh Road, directly opposite the Istana.

PHOTO: Stackedhomes

Cavenagh Fortuna, a freehold residential development at 91 Cavenagh Road, has been launched for sale at a guide price of $60 million.

The guide price works out to $2,599 psf on the net lettable area of 23,089 sq ft, or $1,979 per sq ft on the gross floor area (GFA) of 30,324 sq ft.

JLL is advising the seller in the marketing of Cavenagh Fortuna, and the property will be sold in an Expression of Interest (EOI) exercise.

The District 9 property is situated opposite the Istana, and all 26 units at Cavenagh Fortuna are held by a single corporate owner.

This means that the asset can transfer in one transaction without the collective sale process that a multi-owner development would require.

For a buyer hoping to acquire multiple residential units in a prime freehold development, the usual route is a collective sale.

This process requires at least 80per cent of owners by share value to agree to launch a tender for the sale of the property, this can take 18 months or longer and a sale might be derailed by a single dissenting owner.

The route towards acquiring Cavenagh Fortuna sits outside that process.

According to JLL, the development is owned by a single company incorporated in Singapore, and all 26 units belong to that entity.

Thus, the buyer acquires the whole block through a private negotiation, not a consent exercise. That removes a layer of execution risk that doesn’t factor in a typical collective sale.

However, there is one outstanding legal step to take note.

The development currently sits on two separate land lots and the process of amalgamating them under a single title is underway.

Wee Swee Teow LLP, the appointed solicitors, expect the amalgamation to be completed within a few months, and it is proceeding in parallel with the sale process.

Buyers will need to factor that into their timeline for taking operational control.

Cavenagh Fortuna consists of a single residential block that was completed in the 1990s. The 26-unit development comprises 13 one-bedroom, 10 two-bedroom, and three three-bedroom units.

Unit sizes range from 570 sq ft for a one-bedroom to 2,282 sq ft for a three-bedroom.

The development was comprehensively refurbished between 2014 and 2016, at a reported cost of approximately $6 million.

Over the past five years, the average occupancy at the development is about 98 per cent.

That occupancy rate, sustained across five years through the post-pandemic rental surge and the moderation that followed, is the strongest anchor for a potential buyer on the near-term income stability of the asset.

“The property enjoys strong appeal among both local and expatriate residents for its low-density living and convenience,” says Nicholas Ng, Head of Land and Collective Sales at JLL.

Cavenagh Fortuna is a short walk to The Centrepoint, which is linked directly to the Somerset MRT on the North-South Line (NSL).

From that station, it is one stop to Dhoby Ghaut MRT interchange which connects the NSL, North East Line, and Circle Line.

This proximity to the Orchard Road shopping belt offers a convenient access to a range of amenities, including shopping, food and beverage, entertainment, lifestyle, health and medical, civic and cultural, arts and education facilities.

According to JLL, the development is also an eight-minute drive to the Central Business District, and the area is also served by a connection to the Central Expressway.

In terms of nearby schools, Anglo-Chinese School (Junior) and St. Margaret’s Primary School are within one kilometre of the development.

Other schools in the vicinity include Anglo-Chinese School (Primary), Singapore Chinese Girls’ Primary School, and St Joseph’s Institution Junior.

JLL identifies three primary strategies for whoever acquires the freehold residential asset.

Continuing to operate it as a residential rental development is the most straightforward.

The 98 per cent occupancy track record reduces underwriting risk, and freehold tenure means no lease decay for a holder with a long time horizon.

For an investor who wants immediate yield without repositioning costs, this is the path of least disruption.

On the other hand, applying for a change of use to serviced apartments is another option, and JLL says that URA is prepared to consider this if an application is submitted.

If approved, the new owner could reconfigure the unit mix and potentially earn stronger per-night rates than long-term residential leases achieve.

There is regulatory approval risk involved and execution would require additional capital investment, but the location — a quiet road off the Orchard corridor adjacent to the Istana — is consistent with where serviced apartment demand has historically been strongest in Singapore.

The third option is to bring in a co-living or flexible accommodation operator.

The unit configuration, weighted toward one-bedroom and two-bedroom units, matches the unit types commonly preferred by these short- to long-term accommodation businesses

Redevelopment is technically available under the Residential zoning assigned in the 2025 Master Plan.

But the site’s existing GFA of 30,324 sq ft on a 29,095 sq ft plot implies the current plot ratio is largely utilised.

A buyer who would consider redeveloping the site would need to establish a credible case for GFA uplift through a change-of-use or intensification proposal.

The site’s location directly opposite the Istana may also introduce height restrictions, another regulatory variable that potential buyers should note.

The guide price of $1,979 per sq ft based on the GFA is broadly in line with what individual freehold apartments on Cavenagh Road have achieved in the secondary market.

For example, Cavenagh Court, the nearest comparable freehold development on the same street, has recorded nine resale transactions from January 2022 to December 2025.

Based on caveats, the average resale price for those units transacted is about $1,867 psf.

Meanwhile, resale units at Waterscape at Cavenagh, which is a development further along the Cavenagh Road, have changed hands for about $2,015 psf, based on transactions lodged from January 2022 to February this year.

The development has recorded 42 resale transactions over that period, based on URA caveats.

On that front, the guide price on a GFA basis does not carry a large premium over what individual freehold units on the same street are fetching.

The perspective shifts on a net lettable area basis.

At $2,599 per sq ft, the guide price is above the District 9 freehold median of approximately $2,243 per sq ft for individual apartment resale transactions over the past 12 months.

That price premium reflects Cavenagh Fortuna’s rental occupancy track record, the advantage of acquiring all 26 units without navigating a consent exercise, and the scarcity of prime district freehold whole-block opportunities at this scale.

Direct comparables for a transaction of this structure are limited.

JLL is also marketing a portfolio of 26 freehold units at Residences at Emerald Hill, a development in the same district.

That portfolio of units was launched for sale in April 2026 and are available for sale on an individual basis at guide prices between $4.7 million and $13.4 million per unit, or for a total indicative value of $180 million.

The portfolio of units on the market at Residences at Emerald Hill is a different proposition compared to the sale of Cavenagh Fortuna, since the buyers of the units at Residences at Emerald Hill are acquiring separate units at separate titles.

A buyer at Cavenagh Fortuna is acquiring one asset with full portfolio control at a fraction of the total cost, without negotiating across multiple sellers.

With a guide price of $60 million for Cavenagh Fortuna, the pool of potential buyers will be niche.

Likely buyers include family offices or high-net-worth individuals who might be attracted to the consistent and proven rental yield, the freehold tenure of the asset, and as a generational asset as part of a family portfolio.

With 26 units under a single title, the owner retains the right to subdivide, pass on, or monetise individual units progressively.

Meanwhile, institutional investors with a long time horizon and the appetite for a freehold residential property in a Core Central Region locale would also be a fit.

Co-living or serviced apartment operators are another possibility, though they would need to account for transition costs and the time required to secure a change-of-use approval.

Developers with an eye towards redeveloping the site might not be serious contenders.

At $60 million on a 29,095 sq ft Residential-zoned site, the land rate of $2,062 per sq ft leaves little margin for a developer who also needs to consider construction costs, potential Additional Buyer’s Stamp Duty, and price eventual units competitively against existing freehold stock in the district.

The EOI exercise for the sale of Cavenagh Fortuna closes on July 15.

All 26 units of Cavenagh Fortuna are held by a single corporate owner, allowing the entire asset to be transferred in one transaction without a collective sale process, reducing certain execution risks.

Potential strategies include operating it as a residential rental development, applying for a change of use to serviced apartments, or bringing in a co-living or flexible accommodation operator.

[[nid:736842]]

This article was first published in Stackedhomes.